Japan Corporate Governance Reform

Thesis:

Japan corporate governance reform is going to lead to a re-rating of undervalued companies in Japan.

What is required to make this thesis play out:

1- Japan regulators actually implement measures that compel companies to give money back to shareholders, through repurchases, or dividends.

2- Removal of cross-shareholding that leads to minority shareholders getting fucked the whole time.

Information Supporting Thesis:

1- Japans’s financial services agency (FSA) is busy interviewing investors, and strategising how to compel companies to increase corporate value

.

This picture with source. Read the source, it gives a wonderful overview of their prediction (in 2021) that this would play out, and goes deep into what happens next. Better than my quick simmary so read it.

Summary because you didn’t read it:

In March 2023, the Tokyo Stock Exchange (TSE) unexpectedly issued a guideline to over 3,000 companies, urging them to disclose plans for sustainably increasing their capital returns, specifically targeting those with shares trading below book value. This move marked a significant shift towards addressing capital mismanagement, emphasizing the importance of share price and cost of capital as management considerations. The TSE's directive aimed to foster shareholder engagement and encourage strategies for corporate value creation, highlighting a notable departure from previous reforms focused mainly on corporate governance.

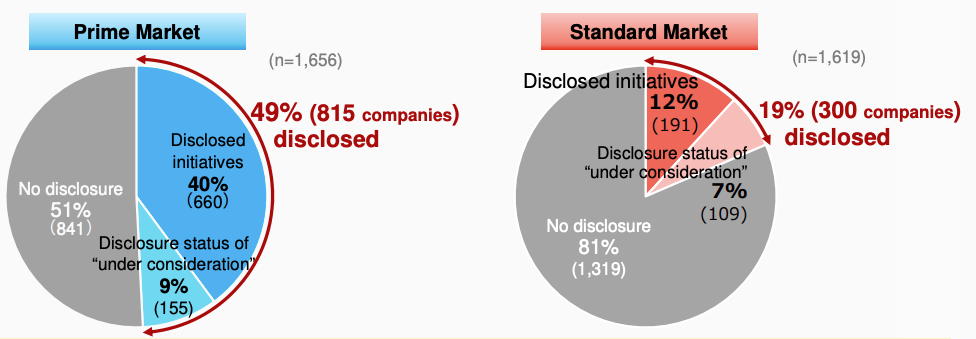

Here’s the list of the companies that DID disclose.

2- This shit is literally working:

The TSE’s March 2023 announcement, dubbed the “Price-to-Book (PBR) Guideline,” had an almost immediate effect on companies especially those listed on the TSE Prime Market. First, they began to undertake share repurchases at record levels, resulting in May 2023 (which is the fiscal year-end reporting period when companies typically announce such measures) seeing the highest buybacks on record.[8] In addition, Japanese companies’ strategic investments, including cross-shareholdings among key clients, group firms and business partners, also continued to fall in the fiscal year ending March 2023, dropping 6% year-on-year, to the lowest level reported since companies were mandated to disclose such investments in 2010.[9] We believe this is a crucial step for many companies contending with low valuations as Japan’s ROE continues to lag overseas peers due to overcapitalized balance sheets.

I’m not going to carry on copying and pasting. I want to use the rest of the article to create strategy to take advantage of what is happening here. Read the document, I promise there is alpha here.

Target & Weight:

Going to add a 10% onto EWJ and then slowly find more Japanese undervalued companies.

Monitor:

Keep track of the regulatory movements.