The 10 Bagger - CorMedix (CRMD)

Oh God no, a Biotech!

I am not betting on a company to pass a clinical trial. That has already happened. I do not take biotech bets on clinical trial stages and the whatnot, I never have. The pitch you are about to read has a product that is already being used successfully.

In the early 2000s, European anesthesiologists faced a recurring problem: reliably reversing deep muscle paralysis after surgery. Their standard agent, neostigmine, often caused bradycardia, nausea, and sometimes left patients with lingering weakness. Then, around 2008, surgeons in Europe began using sugammadex—a novel “molecular cage” that grabbed rocuronium molecules and restored muscle function within minutes. Real‐world reports from London to Madrid showed faster awakenings, fewer respiratory complications, and almost no cholinergic side effects.

Despite these promising European outcomes, U.S. hospitals couldn’t adopt sugammadex immediately. Under FDA rules, even a treatment proven overseas needed its own American clinical trials before any U.S. patient could receive it. In practice, this meant that sugammadex had to be manufactured under U.S. Good Manufacturing Practices and tested in Phase II/III studies across U.S. centers—no shortcuts. Organon (later Merck), and NOT the company I am writing up, launched trials from Boston to San Francisco, comparing sugammadex against neostigmine in diverse American cohorts. They confirmed what their European colleagues had already seen: sugammadex reversed rocuronium blockade in under two minutes on average, with far fewer side effects.

By December 2015, after rigorous U.S. trials and on‐site inspections, the FDA granted approval for Bridion (sugammadex). American anesthesiologists, who had watched European successes from afar, could finally use a standardized, reliably manufactured product. Suddenly, patients at high risk of postoperative breathing problems—whether elderly or with chronic lung disease—could be extubated safely and swiftly.

Sugammadex’s journey highlights three lessons:

Innovations may flourish abroad first, but U.S. patients need FDA‐approved data before they can benefit even when there is conclusive data abroad.

Even proven foreign therapies require domestic trials, ensuring safety and efficacy in American populations.

Leveraging European research—instead of reinventing the molecule—can streamline FDA approval, turning an overseas breakthrough into a lifesaving option for U.S. patients.

Today I will present to you an opportunity with striking parallels:

The Opportunity is CorMedix

Imagine you have a friend named Tom who needs dialysis three times a week. While dialysis is lifesaving, it also means Tom may have a special tube—a central venous catheter (CVC)—permanently inserted into his bloodstream. And every time he’s not getting dialysis, that tube becomes a potential breeding ground for dangerous bacteria. These bacteria can enter Tom’s bloodstream and cause a catheter-related bloodstream infection (CRBSI)—a life-threatening complication that can derail his treatment and even endanger his life.

These infections are shockingly common: up to 25% of patients with CVCs will develop a CRBSI (catheter related blood stream infection), often within the first few months. And the consequences are devastating. Each infection costs the healthcare system an average of $63,000 due to hospitalizations, extra treatments, and extended care. Worse still, about 25% of patients with CRBSIs (catheter related blood stream infections) die within 90 days, making these infections a top cause of death in patients with end-stage renal disease. For patients like Tom—and the healthcare systems that care for them—CRBSIs represent a massive burden that demands a better solution.

To prevent this, hospitals use what’s called a catheter lock solution—a small amount of fluid that’s instilled into the catheter between uses. Think of it like a protective plug: it keeps the tube open and flushes out any lurking bacteria, helping Tom stay safe between dialysis sessions.

In Europe, doctors discovered a clever solution called TauroLock. It combines taurolidine, a natural antimicrobial derived from an amino acid, with citrate (an anticoagulant). Taurolidine acts like a microscopic shield, coating the inside of the catheter to prevent bacteria and fungi from forming colonies, making it much harder for infections to take hold. Over time, TauroLock became so effective that it’s now recommended as a standard-of-care catheter lock in many European guidelines, helping protect countless dialysis patients from life-threatening infections.

I have no proof that CorMedix got the idea from Europe but its likely they did and wondered “Why aren’t we using this here?”. Regardless of whether they got the idea from Europe, CorMedix decided to develop their own solution for U.S. patients. Instead of using citrate, they paired taurolidine with heparin, an anticoagulant more commonly used in the U.S. dialysis setting. The result was DefenCath, a catheter lock solution designed to fight infections and keep the catheter open.

After rigorous clinical trials—including a study that showed a 71% reduction in infections—DefenCath won FDA approval in November 2023. It’s now making its way into hospitals and dialysis clinics (its biggest market) across America, giving patients like Tom a fighting chance against dangerous infections that can sideline their treatment and threaten their lives.

CRBSI (Catheter-Related Bloodstream Infections) are a major problem in patients with central venous catheters, with up to 25% of patients developing an infection—often within the first few months. These infections cost the healthcare system an estimated $63,000 per case and represent a significant burden both financially and clinically. DefenCath addresses this problem.

TauroLock is widely used in Europe, especially for high-risk patients, and has demonstrated strong efficacy in preventing catheter-related infections in RWE (Real World Evidence) studies. DefenCath takes a similar approach, using taurolidine but pairing it with heparin—a common anticoagulant in U.S. dialysis settings—instead of citrate. Clinical Studies should look very similar for Defencath.

Real-world evidence (RWE) from European studies on taurolidine-based catheter lock solutions like TauroLock shows substantial efficacy in preventing infections. Given that DefenCath uses the same active ingredient—taurolidine—but pairs it with heparin instead of citrate (just an anticoagulant), I expect DefenCath’s results to be very similar to that of Taurolock. RWE studies for DefenCath (coming out next month) should look almost identical to its clinical studies- incentivizing more Medicare support, and incentivizing insurers to foot the entire bill to save money on their patients.

Worst-Case Scenario on CorMedix

Allow me to first peak your interest with my absolute worst-case scenario anaylsis on CorMedix. I will explain all the nitty gritty details afterwards, which are very important to understand in order to build conviction.

My worst worst worst case gives CorMedix a terminal value of $1.8Bn. Double its current market price. I also don’t calculate any NPV for 2025 or 2026 even though 2026 could be a very big year for CorMedix.

You’ll fall off your chair when you see my base case.

My worst-case scenario assumptions include:

Market Penetration: I assume DefenCath captures only 10% of its Total Addressable Market (TAM) by the end of 2027—a very conservative estimate considering CorMedix has already achieved approximately 2% penetration from one of the smallest dialysis organizations and has already signed up the others.

No TAM Penetration Growth: I assume the TAM penetration remains flat beyond 2027, despite strong clinical results and DefenCath’s compelling value proposition as a life-saving therapy.

Severe Price Erosion: I assume DefenCath faces significant price erosion from the TDAPA price-drop off (which I will explain nicely later), due to failed negotiations with Medicare Advantage plans, increased hospital price pressures, and hypothetical competition (though no direct competitors currently exist). Even in a bear-case scenario, pricing would likely remain well above the level I assume here.

High Operating Expenses: I assume operating expenses remain elevated, significantly higher than the company’s current trajectory and guidance would suggest.

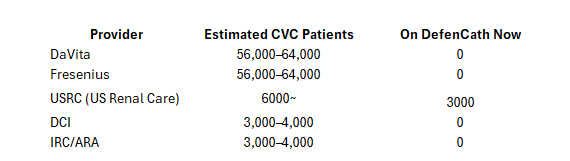

Large Dialysis Organizations (LDOs)

CorMedix currently has agreements with four of the five largest dialysis organizations- which represent some 70%~ of their TAM. They are tabled below. The rest of their TAM will come from hospitals, but will take longer to roll out (they already have sales-teams in place, but I don’t even incorporate this into my analysis).

Of these five (below), US Renal Care is the only one who has implemented and ordered- the others are still rolling out and should roll out before year.

CorMedix already has a contract with either DaVita or Fresenius, but they have not disclosed which one. If only half of the CVC patients from either of them use DefenCath my worst-case scenario is null and void.

TAM and DefenCath Studies

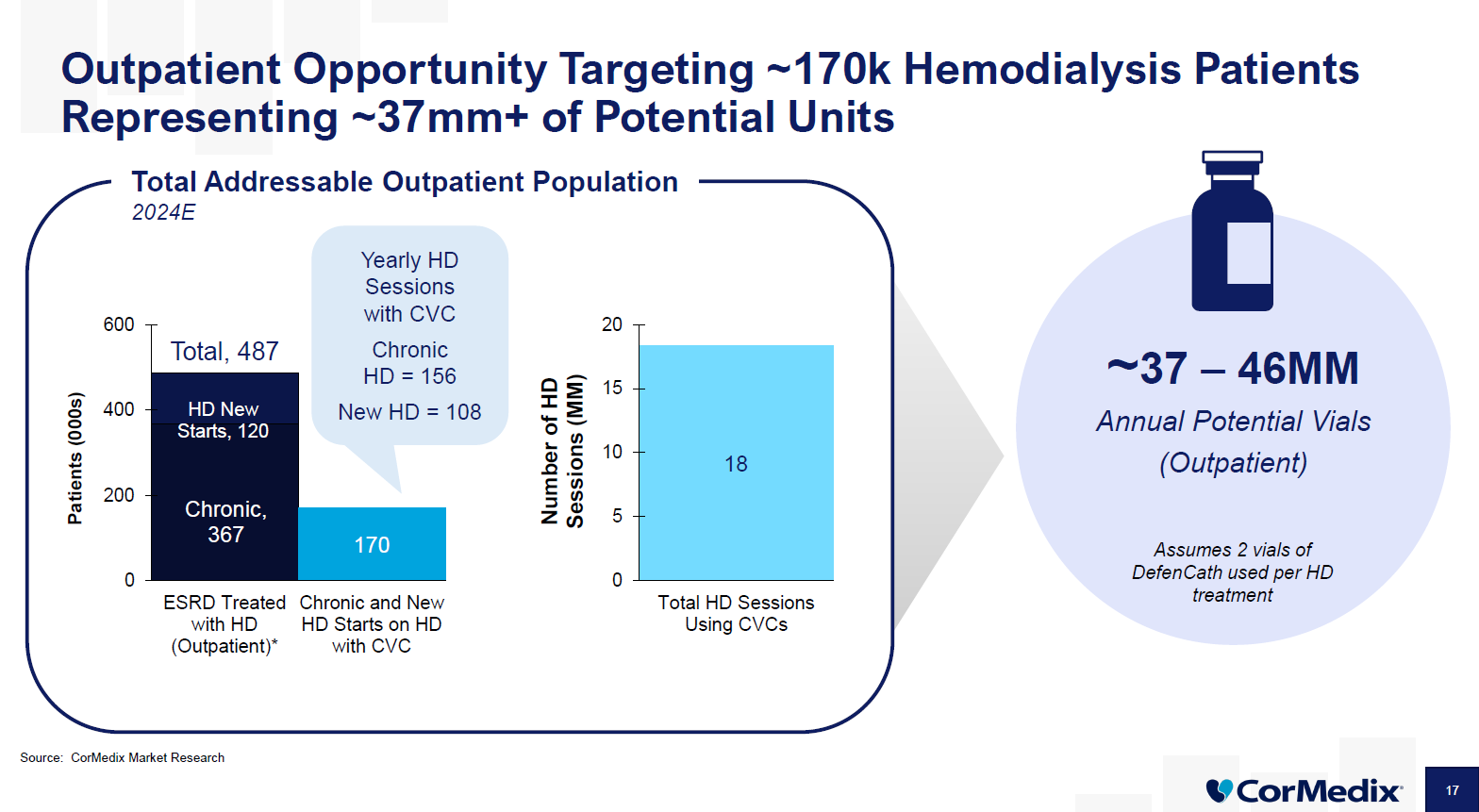

CorMedix estimates its Total Addressable Market (TAM) at around 170,000 patients—mostly dialysis patients who rely on central venous catheters. My own research supports this figure, landing just a bit lower but well within the same ballpark.

Now, here’s where it gets fun: CorMedix has already signed contracts that cover about 70% of this TAM. The clinics are onboard and it’s just a matter of rolling out the product and getting patients started on DefenCath. That rollout is happening now, and investors are hungry for details. Every earnings call is filled with questions about what the dialysis organizations are saying, how many patients are lined up, and how quickly those patients are being converted to DefenCath.

Personally, I’m not focused on the next quarter’s numbers—too many variables and short-term noise. Instead, I’m looking two and a half years down the road, at the end of 2027. By then, I’m confident that at least 10,000 patients will be using DefenCath—that’s the number my worst-case scenario is based on. And frankly, given the pace of adoption and the scale of the need, I think that’s its too conservative an estimate.

The reason I’m so confident about DefenCath’s potential is because we’ve already seen its European cousin (TauroLock) used very effectively to reduce catheter-related bloodstream infections (CRBSIs) in Europe. I’ll share some real-world evidence case studies later, but the bottom line is that TauroLock has been saving lives and preventing costly infections for years.

DefenCath uses the same main ingredient—taurolidine. The difference is that instead of combining taurolidine with citrate (like TauroLock does), DefenCath pairs it with heparin, an anticoagulant that’s more commonly used in the U.S. dialysis setting. Both citrate and heparin are standard anticoagulants used in catheter locks across Europe and the U.S., so this switch doesn’t change the core infection-fighting benefit.

At the heart of this is a serious, expensive problem: ESRD patients on dialysis with catheters face devastating infections, and each one costs the healthcare system an average of $63,000. DefenCath offers a solution that could save Medicare and insurance companies a fortune—giving CorMedix real negotiating power to maintain its current price of $250 per vial. (I’ll get into pricing dynamics later.)

CorMedix is currently awaiting new data from its real-world evidence (RWE) study, expected to be released next month in July. I believe these RWE results will align closely with the clinical trials—just like the numerous European RWE studies on TauroLock, which have consistently confirmed its effectiveness. Since DefenCath is so similar, this new data could give CorMedix a powerful hand when negotiating with Medicare to maintain or even enhance its reimbursement structure. (I’ll unpack that more in a bit.)

Here’s a glimpse from one of the European studies:

https://pmc.ncbi.nlm.nih.gov/articles/PMC4224385/

Price erosion (TDAPA roll off)

What is TDAPA, and why does it matter for DefenCath?

When a new drug like DefenCath launches, Medicare offers a special incentive program called the Transitional Drug Add-On Payment Adjustment (TDAPA) to encourage clinics to adopt innovative treatments.

Think of TDAPA as a welcome mat for new therapies:

For the first two years of launch, Medicare pays clinics the full price of the drug on top of their regular payments—giving clinics a risk-free way to try out the new therapy.

Starting in years three to five, Medicare payments begin to phase down: instead of paying full price, Medicare covers 65% of the prior year’s drug spend per treatment. This means clinics start to see declining reimbursement for the product.

After year six, the extra payments go away completely, and the product is fully integrated into the dialysis bundle. This shifts all pricing and reimbursement risk to the provider, putting significant price pressure on the drug.

Where is DefenCath on this timeline?

FDA Approval: November 2023.

Outpatient Commercial Launch (TDAPA Start): July 2024.

Years 1-2 (2024-2026): We are currently in the initial TDAPA phase—clinics get full reimbursement, making it financially attractive to try DefenCath.

Years 3-5 (2026-2029): Payments will drop to 65% of the prior year’s drug spend per treatment, meaning prices will start to erode.

Year 6+ (2029 onwards): The product is fully absorbed into the dialysis bundle, with no add-on payments and heightened price pressure.

My worst-case scenario assumes a much steeper drop off than typically happens. Volume does not directly effect price during these periods. I

In my worst-case scenario, I assume prices drop all the way to $50 per vial and only 10,000 patients are using DefenCath. That’s a pretty harsh scenario—one where clinics have to fully absorb the cost without any carve-out support from Medicare.

Here’s why that matters: Medicare typically pays dialysis clinics a single bundled payment per treatment that covers everything—staff, supplies, and most medications. But sometimes, for new, innovative therapies like DefenCath, Medicare or Medicare Advantage plans agree to “carve out” the cost of the drug from the bundle. That means they pay separately for the drug, so the clinic doesn’t have to eat the cost out of its bundled payment.

There are precedents for Medicare carving out drugs that clearly save them money in the long run. And with DefenCath’s potential to slash infection rates and reduce hospitalizations—each CRBSI costs the system around $63,000—I think it’s definitely possible that Medicare would agree to carve out DefenCath which sells for $250 per vial.

But for the sake of being conservative, I’m sticking with my $50 per vial assumption in the worst-case scenario. It pays to be conservative.

Price Erosion: Why I’m Not Too Worried

First, CorMedix’s management team is well aware of this challenge. From day one, they’ve been preparing to defend DefenCath’s value by showing that it saves the healthcare system money. That’s where their real-world evidence (RWE) study, to be released next month, comes in:

Over 2,000 patients enrolled at US Renal Care are being tracked on critical metrics like infection rates, hospitalizations, antibiotic use, and mortality.

These data points are crucial for proving that DefenCath dramatically cuts downstream costs, making it a financial no-brainer even at higher prices.

Second, let’s talk about Medicare Advantage—the fastest-growing share of dialysis reimbursement. Medicare Advantage plans cover both dialysis and the hospitalizations that come with infections:

Every CRBSI costs about $63,000 per case; DefenCath at $250 per vial is a rounding error by comparison.

CorMedix plans to leverage RWE data to negotiate directly with these plans, setting sustainable prices that reflect the real savings DefenCath delivers.

And let’s not forget the barriers to entry:

DefenCath is protected by regulatory exclusivity through 2033.

No direct competitors have FDA approval to sell a similar taurolidine catheter lock solution in the U.S.

Hospitals and dialysis chains have one option to prevent these infections: DefenCath.

Okay so according to Substack I’m reaching ‘email length limit’ and will have to make a part 2 of this. I’ll leave this here for now,

and in Part 2 I’ll dive into more detail on TDAPA price roll off, rollout progress, and other aspects that are interesting to understand in depth. I’ll also go into more depth explaining my Base case scenario…

Please actually comment and restack this if you found it interesting. It will help drive the algorithm to recommend this post, and help incentivize me to write on more opportunities I find.

Well done. Very detailed.

Written clearly and well-researched. Great find